I don’t know about you, I know it is important to keep up to date on the companies, in which I am invested. However, sometimes I am just too busy or just too lazy to read them. They aren’t the most interesting ‘literature’ available, and more often I will just glance through the financial highlights.

Well, in lieu of the ‘dull’ earning reports, there is always Netflix, Prime, Disney+ or YouTube.

In addition, the past couple of years have not been kind to many companies, as the pandemic affected them negatively. So it can be rather disheartening to read through the long list of woes and cautious outlooks. Perhaps it is my mind mentally avoiding all the negative information… which is why I having been reading these reports as much.

In my previous post (see below), I mentioned about two stocks in my portfolio that have improving outlooks or earnings. Namely, CapitaLand Ascott Trust & Straco Corporation Ltd.

“Recovery” stocks in my portfolio – Will the rainbow finally be here? (read here)

While going through the other companies’ filings which I am vested in, it is good to know that more companies are starting to turn the corner after years of declining profits. Of course, there are other solid companies that continue to do well (very well)… eg. Mastercard, Alphabet, DBS, and ParkwayLife Reit….to name a few.

For the former group, although their earnings have started to improve, it appears that the stock prices have yet to ‘catch’ up. Then again, the stock is not the company and it might finally reflect the value after the long term. It can be argued that these are not the top-tier growth stocks, but I do believe they have their strengths. I have a substantial percentage of my portfolio in Hong Kong-listed stocks and quite a number of these stocks are Hong Kong-listed.

PDD Holdings Inc

I find PDD’s earnings rather erratic (esp. for the free cash flow). See below. Still, I can see it is improving overall (eg. EPS).

After the terrible earnings report in Q12022, earnings seem to be getting better. Its shopping app continues gaining in popularity while China continues to shed more light on its potential stimulus plans, which may have “big impact. PDD’s Temu app has pretty much gone viral in the U.S. Indeed, consumer appetite for incredibly low-cost discretionary goods could stay strong as inflation and macro headwinds continue to impair our ability to spend on nice-to-have goods.

For 3Q2023:

1) Total revenues in the quarter were RMB68,840.4 million (US$19,435.4 million), an increase of 94% from RMB35,504.3 million in the same quarter of 2022.

2) Operating profit in the quarter was RMB16,656.0 million (US$2,282.9 million), an increase of 60% from RMB10,436.6 million in the same quarter of 2022.

3) Net income attributable to ordinary shareholders in the quarter was RMB15,537.1 million (US$2,129.5 million), an increase of 47% from RMB10,588.6 million in the same quarter of 2022.

The share price is up almost 320% from the lows in March 2022. Its P/E Ratio at 30.79 is rathe high though. Well, the earnings is much better compared to Alibaba’s recent earnings (and Tencent March 2023 earnings).

Lam Soon (Hong Kong) Ltd

The EPS chart of Lam Soon has not been pretty. See below.

Annual profit has been trending down since 2019.

As stated by the Chairman in its 2023 Annual Report (emphasis mine): “FY22/23 marked a challenging year for the Group, as the negative impact of global geopolitical tensions and Covid-19 policies in our core markets reverberated across all of our businesses. Despite the diversified nature of our Group, we were not completely immune to raw material cost pressures and dampened market demand.

The Group posted a profit of HK$85 million against revenues of HK$5,119 million during the financial year, representing declines of 67% and 16% respectively against last year.“

However, there has been an uptick in the free cash flow in the recent quarter.

In addition, the company made an announcement on 2 Feb 2024 titled “POSITIVE PROFIT ALERT“, and to quote (emphasis mine):

“The Board of Directors (the “Board”) of the Company wishes to inform the shareholders of the Company and potential investors that, based on the preliminary review of the unaudited consolidated management accounts of the Group for the six months ended 31 December 2023 and the information currently available to the Board, the Group is expected to record a net profit in a range of approximately HK$120 million to HK$140 million for the six months ended 31 December 2023, as compared to the net profit of HK$42 million for the previous corresponding period.

The increase in net profit for the six months ended 31 December 2023 as compared to the previous corresponding period was mainly attributable to favourable wheat costs and edible oil raw material costs resulting from stabilised global supply, and sales volume growth and product mix improvement.

The Company is still in the process of finalising its interim results for the six months ended 31 December 2023.”

The share price has been beaten down over the years and has only slightly improved. It is down more than 46% from the Nov 2021 level.

Link Real Estate Investment Trust

In its 1H 2023/2024 Interim Presentation in Nov 2023, revenue and NPI have increased YOY while gearning is down YOY.

For the Hong Kong Retail segment, it has maintained 98% occupancy and achieved 8.7% rental reversion. The average unit rent has also surpassed pre-Covid level.

The Hong Kong Car Parks and Related Business segment, revenue is up 5.2% YOY, income is up 5.3% YOY.

Its investment in Singapore Retail has 99.3% occupancy.

Australia Retail has 98.1% occupancy.

Other segments like International Office, Mainland China Retail, Mainland China Logistics are also recovering and doing well.

The share price is still depressed, down almost 50% from its June 2021 level.

Well, I am still slowly reading up on some of the other earning reports of the companies which I am vested in. It is a welcome change for some when situations start getting better.

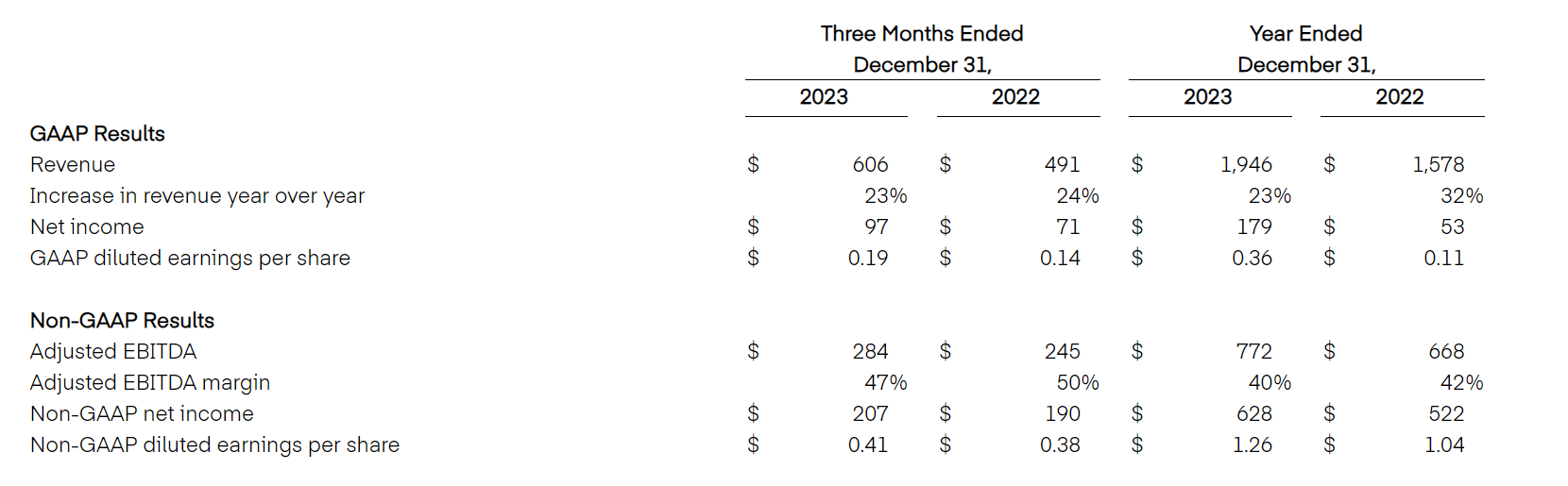

Trade Desk

Fourth Quarter and Fiscal Year 2023 Financial Results

Jeff Green, founder and CEO of The Trade Desk (emphasis mine): “Once again The Trade Desk outpaced nearly all areas of digital advertising in 2023, with $1.95 billion of revenue representing 23% growth year over year and a record $9.6 billion of spend on our platform. At the same time, we continue to generate significant profitability and cash flow, which allows us to remain at the bleeding edge of our industry, with innovations such as Kokai. Our results are testament to the growing value that advertisers are placing on the open internet versus the limitations of walled gardens,”

Financial Guidance:

First Quarter 2024 outlook summary:

- Revenue at least $478 million

- Adjusted EBITDA of approximately $130 million

Trade Desk Jumps As Internet TV Drives Strong Revenue Outlook (read here)

The share price is up almost 100% form the Dec 2022 level. However, with a P/E ratio of almost 302$ it maybe too expensive for me.

Thank you for reading.

Webull

Sign up for a Webull account via my referral link and get up to $2,500 worth of Tesla shares.

StocksCafe

FYI I find StocksCafe useful for the tracking of my own portfolio, and I especially like to use it to track my portfolio stock dividend/bond interest payouts (projected and due). You can use my referral code: apenquotes. Just click here. Upon signing up using the referral code, you will get to enjoy being a Trial Global Friend of StocksCafe and test out all features for free for one month!

Please follow me at StocksCafe, via my StocksCafe profile page.

Tiger Brokers

For the Singapore market, Tiger Brokers currently waive the minimum fee and only charge a 0.08% trading fee. This drastically reduces your cost as the minimum fee from other brokers (ranging from SGD 8 such as FSMOne and SCB, to SGD 25 for local brokerages) does add up and can eat into your returns.

Tiger Broker Referral Code:: GPE59H

I would like to invite you to start investing with Tiger Brokers so you can claim your welcome bundle.

Sign up here.

FSMOne.com

Typically I use FSMOne.com to invest in funds & ETFs (including money market funds).

If you do not have an account, you can sign up here. Please use my FSMOne referral code: P0031127, when you sign up.

Wise Card

Traveling overseas? The Wise card lets you spend money around the world with low conversion fees and zero transaction fees. Please use my referral link to sign up for one.

Shopee

I have been using Shopee for a while and think you will like it as much as I do.

Get $10.00 off your first purchase using my code DARREB52.

Download Shopee now and enjoy hot deals at the best prices! Click here.

Happy shopping!

Gemini

As stated by MoneySmart on Jan 22, if you’re looking to optimise trading your crypto with relatively low fees, simple-to-grasp expert UI and ease of purchase with Singapore dollars. then the best crypto exchange in Singapore is Gemini,

If you do not have an account, you can sign up here using my referral link. After you have signed up, once you buy or sell US$100 or more (or 100 USD equivalent of your domestic currency) within 30 days of creating your account, your account will be credited US$10 (or 10 USD equivalent of your domestic currency) worth of bitcoin.