It is common for many to do a review of their portfolio at the end or start of the year, and I am no exception. It is good to be retrospective and take stock of what happened in the past year.

The good thing about having a blog (or a journal) is that I can always go back and check what I was thinking about in the past. When I read back my previous posts during the period from the end of 2021 to the start of 2022, I realized that I was generally rather pessimistic about the coming year 2022.

Thoughts on my Portfolio (Nov 21) (read here) – Written on 8 Nov 2021

To quote the post above:

“In a way, I am using the income-generating portion as a ‘base’ from which to slowly grow the other portions. Although, almost every month I do reinvest part of the dividends/interests received into dividend stocks as well.

Generally, I feel that valuations in the US Growth stocks are rich, and values can be found in Chinese tech stocks at the moment. Many renowned investors (Charlie Munger, Monish Prabai, Ray Dalio, etc) have waded into this sector in 2021.”

Short post for the start of 2022 (read here) – Written on 2 Jan 2022

To quote the post above:

“With the rich valuation of the US markets, I do not foresee much investing in the coming weeks or months…

Plan for 2022 (Investment)

To be frank, I do not have a very clear plan at the moment. I reckon I am still waiting for the markets to direct my actions….

However call me superstitious, as per my horoscope (fire dragon) reading for 2022, it is not advisable to bet big on risky assets in 2022.”

The most underrated key to investing and time for me to revisit it in 2022 (read here) – Written on 18 Jan 2022

To quote the post above:

“2) Valuation: It could also be the fact that from many valuation indicators, the US markets do appear overvalued (from a P/E valuation perspective). Singapore market (from a P/B valuation perspective) appear slightly below or full valued, while the Hong Kong market is undervalued (from a P/B valuation perspective) if we can accept the regulatory risks.

I still believe that if the US markets sneeze, the other bourses will also catch a cold. Well, these days, when the China markets sneeze, many markets elsewhere also appear to be affected.

So with the 3 or 4 impending rate hikes in the US; and high valuation and potential pull-backs… I would say the odds are good that we can find better opportunities moving forward in 2022 and even 2023.“

While it is normal for me to look at the overall net worth, I think there are other better ways to evaluate.

Overall my net worth increased only slightly in 2022. In fact, gains from my active income and passive income are mostly negated by the (unrealized) losses in my portfolio. That being said, there are many things that I reckoned I have done well or as intended.

Low negative XIRR

XIRR: To calculate returns on investments where there are multiple transactions taking place in different times. Full form of XIRR is Extended Internal Rate of Return.

I don’t consider myself good at market timing, and I still believe in DCA. However, given the relatively high valuation and generally negative outlook, and impending rate hikes in the US, back at the end of 2021/start of 2022, I decided to delay and space out my investments longer.

For instance, for the first half of the year (2022), there were lesser investments with smaller amounts as compared to the later part of the year. It could be argued that 2023 might provide better opportunities, but who knows. However, on a yearly basis, for 2022 I am glad that I delayed most of the DCAs. See below.

Digicore Reit’s stock price tanked in 2022. Many of the tech stocks in my portfolio also did not fare well in 2022, stock price wise (eg. Alibaba, and subsequently Tencent).

It is not that I did not invest in them (tech/growth stocks), yes, overall the amount invested relatively speaking is smaller than the amount invested in dividend stocks. However, I guess the smaller allocation in growth stock as compared to my dividend stocks could also be due to the bigger stock price drop for growth stocks (even Digicore Reit which is not technically a growth stock behaved like one, price-wise).

Of course, I might be better off overall by just selling everything and staying out of the market for the whole of 2022. However, that is a tad too extreme and I likely would not do it if I were to go back in time.

For the year 2022, the overall XIRR though negative is not that bad.

I generally still think the Hong Kong (dividend and growth) stocks offered better value and invested more there in 2022. Ultimately 2022 was a better year in terms of price appreciation for the Singapore market.

Hope with China and Hong Kong re-openings things will get better in the later part of 2023. Earnings for these companies will finally see substantial improvement.

2022 may turn out to be a good year

If we believe that markets move in cycles due to the various external factors (interest rates, war, Covid) and internal factors (earnings & innovations of companies, etc)… then perhaps from a long-term perspective, the year 2022 would lay the foundation for subsequent good years for equities (eg. if not 2023 then 2024 and beyond).

While many would focus on the stock prices and their eventual net worth and fear more future rate hikes by the US Federal Reserve and ongoing world issues like Covid-19 (cases mounting in China), the ongoing war in Ukraine, and worldwide recession; not that many mention valuations.

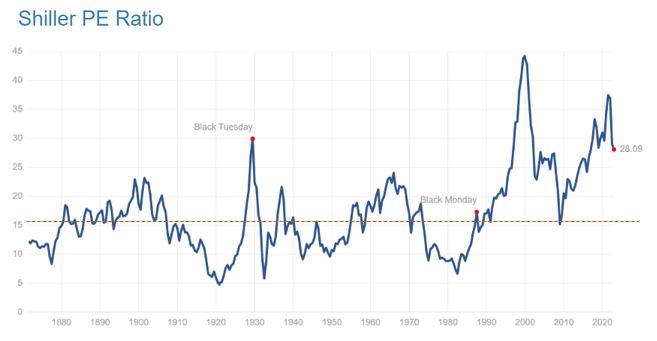

For the S&P 500, the current Shiller PE Ratio (on 30 Dec 2022) is 28.09. See above. With the median PE at 15.90, it is still technically not cheap. However, when viewed in context, the value has not been cheap for a very long time, only reaching near or below that level during the GFC in 2008/2009 and during the early 1990s.

In recent years, during the lows of the March 2020 market crash, the Shiller PE ratio was 24.82. Currently, we are close to the levels seen in May 2020 (27.33) and June 2020 (28.84).

I reckon the US Federal Reserve has been getting better at using the interest rate tool, qualitative easing (QE) or qualitative tightening (QT). Would we ever see the lows in S&P500 during the 2008/2009 GFC? Would the US Federal Reserve not do anything (keeping in mind that the money printer is still very much there, with the lure of cheap money)?

Over in Hong Kong, Hang Seng’s PE hit a low of 6.1 in 1984 and a high of 29.7 in 2000. Its historical average is 12.5 times earnings. The Hang Seng P/E ratio on 31 Dec 2022 is 7.16. The current PE ratio is lower than the historical average.

Perhaps a better gauge of the Hang Seng Index valuation will be via its Price to Book ratio, which is currently at 0.92 (on 4 Jan 2023). In 30 years, it was below 1 only in 1998, 2016, and of course in March 2020 (till probably now).

Hang Seng index hits 2008 lows: Chinese equity ETFs to watch (read here)

Hong Kong: HANG SENG INDEX (.HSI) now trading below its net asset value for only the third time in almost 30 years (read here)

Here in Singapore, the SPDR Straits Times Index ETF (ES3.SI) has a current Price/Book value of 1.11. Since 1980, the P/B ratio of Singapore’s stock market has averaged 1.44. Right now, it’s hovering just slightly above 1. The current level is below the historical average. This also means that investors think that, as a whole, companies traded on the Singapore stock market are only worth as much as their net assets.

I watched this Youtube video episode with Adam Khoo as the guest (watch here), and I tend to agree with that part of what he said about the year 2022, which might turn out to be a good year if you are a long-term buy-and-hold investor, and have invested money you do not need urgently in the short term.

Going into the new year with more stock holdings and increasing dividend income

While my net worth did not look (ahem) good, my stock holdings have actually increased and my passive dividend/interest income has reached a new high.

Price is just one aspect of the equation. Unless I am nearing retirement and need to liquidate my positions, otherwise I should not be too concerned about price volatility.

And if we really think about the concept of money – it is after all a concept (fiction) based on trust, not backed by gold, silver or any other commodity. Money only works because we all agree to believe in it.

I would recommend reading the book titled “Money: The True Story of a Made-Up Thing” by Jacob Goldstein.

“Money feels cold and mathematical and outside the realm of fuzzy human relationships. It isn’t. Money is a made-up thing, a shared fiction. Money is fundamentally, unalterably social. The social part of money—the “shared” in “shared fiction”—is exactly what makes it money. Otherwise, it’s just a chunk of metal, or a piece of paper, or, in the case of most money today, just a number stored on a bank’s computers.”

― Jacob Goldstein, Money: The True Story of a Made-Up Thing

“Remember the first seven words of that last sentence: “Everyone believes that it will hold up.” They are the essence of banking (and, for that matter, of money). If everyone believes a bank will hold up, it will almost certainly hold up. If, on the other hand, people think a bank is going to fail, it will fail—even if its finances are in great shape.”

― Jacob Goldstein, Money: The True Story of a Made-Up Thing

Unlike the feeling at the end of 2021 / start of 2022, I do believe in continuing to DCA at a normal rate this year and investing more during the dips (or when trends reverse). I have always been telling myself to go more into growth stocks, but I tend to favor dividend stocks especially now given their increasing yield and more so for Hong Kong-listed dividend stocks.

If at the start of 2022, I see more value in HK growth stocks (cough cough Alibaba cough…), then perhaps I can be persuaded to be more aggressive in 2023 in my purchases. BTW I liquidated my Alibaba position (9988.HK) in 2022 and switched to Tencent (0700.HK). I have recently added a bit more (0700.HK).

Currently, US0listed and HK-listed growth stocks (eg. Alphabet and Tencent) have PE ratios below 20, and even Pinduoduo is at a low 20 to 30 PE. If one is to not consider the R&D expenses (necessary for capturing market shares as growth companies), these are indeed good valuations, brought about by the negativity of the high-interest rate environment.

Having experienced the Financial crisis of 2008, the European debt crisis of 2009-2010, Coronavirus crash of 2020, US-China tension, QE, QT, etc…it is probably more important to keep on buying on a regular basis, keeping to my barbell investment principle and slowly build up my growth and dividend portfolios, while keeping an eye on the fundamentals of the companies invested. After all, to quote Adam Khoo again, even God couldn’t beat dollar-cost averaging (read here).

If we are to extend the idea of pendulum and cycles by Howard Marks, I do believe we are sensing much pessimism and negativity now. Trees don’t grow to the sky and things seldom go to zero… Many stocks are at good valuation with moods generally negative.

It might be hard to see better days now, but we should not wait for the sky to be all clear to invest.

Hold on.

“[On the consistent swinging of the pendulum between fear and greed] The significance of all this is the opportunity it offers to those who recognize what is happening and see the implications. At one extreme of the pendulum – the darkest of times – it takes analytical ability, objectivity, resolve, even imagination, to think things will ever get better. The few people who possess those qualities can make unusual profits with low risk. But at the other extreme, when everyone assumes and prices in the impossible – improvement forever – the stage is set for painful losses. It all goes together. None of these is an isolated event or a chance occurrence. Rather, they’re all elements in a recurring pattern that can be understood and profited from.” Howard Marks

Thank you for reading. Happy New Year everyone.

StocksCafe

FYI I find StocksCafe useful for the tracking of my own portfolio, and especially like to use it to track my portfolio stock dividend/bond interest payouts (projected and due). You can use my referral code: apenquotes. Just click here. Upon signing up using the referral code, you will get to enjoy being a Trial Global Friend of StocksCafe and test out all features for free for one month!

Please follow me at StocksCafe, via my StocksCafe profile page.

Tiger Brokers

For the Singapore market, Tiger Brokers currently waive the minimum fee and only charge a 0.08% trading fee. This drastically reduces your cost as the minimum fee from other brokers (ranging from SGD 8 such as FSMOne and SCB, to SGD 25 for local brokerages) does add up and can eat into your returns.

Tiger Broker Referral Code:: GPE59H

Promotion Period: 16:00 06/12/2022 – 15:00 28/02/2023(SGT)

Sign up and open an account with Tiger Brokers (Singapore) during the promotional period to receive a free GoPro Share (NASDAQ: GPRO), 365 Days of unlimited commission-free trades for HK, SG, and China A stocks, 180 Days of unlimited commission-free trades for U.S stocks, 5 commission-free trades for options within 30 Days and 1 month Ryde+ subscription.

Sign up here.

FSMOne.com

Typically I use FSMOne.com to invest in funds & ETFs (including money market funds).

If you do not have an account, you can sign up here. Please use my FSMOne referral code: P0031127, when you sign up.

Shopee

I have been using Shopee for a while and think you will like it as much as I do.

Get $10.00 off your first purchase using my code DARREB52.

Download Shopee now and enjoy hot deals at the best prices! Click here.

Happy shopping!

Gemini

As stated by MoneySmart on Jan 22, if you’re looking to optimise trading your crypto with relatively low fees, simple-to-grasp expert UI and ease of purchase with Singapore dollars. then the best crypto exchange in Singapore is Gemini,

If you do not have an account, you can sign up here using my referral link. After you have signed up, once you buy or sell US$100 or more (or 100 USD equivalent of your domestic currency) within 30 days of creating your account, your account will be credited US$10 (or 10 USD equivalent of your domestic currency) worth of bitcoin.

Pingback: 2023: A new Dawn for Chinese / Hong Kong Stocks? A case study of Tencent | A Pen Quotes