“There is only one combination of facts that makes it advisable for a company to repurchase its shares: First, the company has available funds — cash plus sensible borrowing capacity — beyond the near-term needs of the business and, second, finds its stock selling in the market below its intrinsic value, conservatively calculated.”

— Warren Buffett, 2000

Sometime ago, I stumbled across a listed company called GP Industries Ltd. According to their 2014-2015 Annual Report, the company holds a 62.2% interest in GP Batteries International Limited. GP Batteries is engaged in the development, manufacture and marketing of batteries and related products.

GP Industries is principally engaged in the development, manufacture and marketing of electronic and acoustic products. In addition, GP Industries also manufactures automotive wire harness products.

Most of the company’s revenue is from batteries (see below).

At that time, I gave GP Industries a second thought because their products are low-tech, easy to understand and disposable (repetitive nature of the product that is relatively immune from technological obsolescence and recessions). I vividly recall GP rechargable lithium ion batteries (which I see in supermarkets). Some say rechargable lithium ion batteries will dominate the market. Of course, I also remembered that Warren Buffett in Nov 2014, decided to buy the Duracell battery brand from Procter & Gamble in a multi-billion dollar deal. (read here)

Unfortunately, for GP Batteries International Limited financial performance in FY2015 as compared to FY2014: Sales of primary batteries increased by 7% and sales of rechargeable batteries declined by 8%. Think I would need to rethink the “rechargable lithium ion batteries will dominate the market” theory in GP Industries’ case.

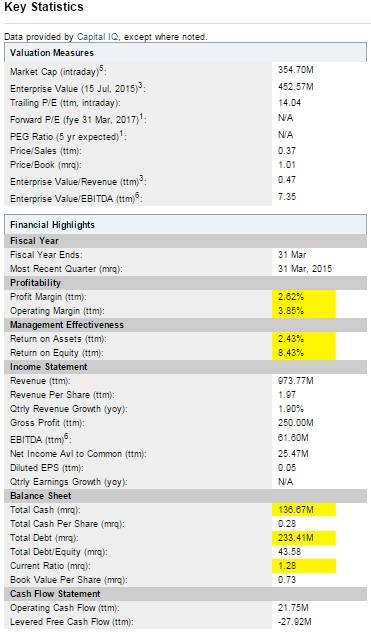

Eventually, what stopped me from investigating further is their poor financial fundamentals. Let me elaborate (don’t have the data from back then, let’s use what I can find now).

As you can see;

- The profit margin and operating margin are not impressive (too low for my liking).

- Similarly, Return on Assets and Return on Equity are too low (would have preferred ROE to be at least 20%).

- The Current Ratio is also not ideal at 1.28. Acceptable current ratios vary from industry to industry and are generally between 1.5 and 3 for healthy businesses.

- The killer is the large amount of debt, after deducting total cash, there would still be SGD96.74 million of debt.

Nevertheless, the price to book is not high (almost 1), and EV/EBITDA at 7.35 is less than 10 (as a rule of thumb, any EV/EBITDA below 10 is the sign of a good value. It might be considered undervalued to some).

The free cash flow is also not trending upwards over the years (see below).

The revenue has over the years been relatively flat and the net income is erratic (not consistently trending up). (see below)

The earnings per share over the years is also erratic (not consistently trending up). In addition, the EPS growth (5 years) is a negative 3.1. (see below)

However, GP Industries caught my attention due to one reason, there have been active share buy backs. ‘Active’, this word in this case seem to be an under-statement. Every other day, I can find records of share buy back (read here). Why don’t they just buy most of these shares at one go? Or buy all…. :p Hmmm…High Frequency trading a la company share buyback version.

“Stock buybacks are the simplest and best way a company can reward its investors,” Peter Lynch

I do not dispute the fact that share buybacks has always been one of the top things I look for when assessing the investment merits of a stock. As the number of stocks outstanding get reduced, the Earnings per Share would correspondingly increase. Financial engineering 101.

Having said that, although share buybacks are good, we still need to look hard to assess whether management is shareholder friendly. It is just not that simple eg. buybacks are good – period.

As mentioned in Warren Buffett’s quote at the beginning of this post about share repurchase:

- First, the company has available funds.

- Finds its stock selling in the market below its intrinsic value, conservatively calculated.

When companies buy back shares when it has net debt, less money is allocated to debt repayment, and when they buy back shares at an inflated price, shareholder value is destroyed.

The share price of GP has been steadily trending up, so one wonders if the share repurchases are indeed wise and cheap.

This is unlike what Sarine Technologies Ltd management is doing (read here). They seem to buy shares with clockwork precision when stock prices dip (right after bad news).

Listen To Buffett: All Share Buybacks Weren’t Created Equal (read here)

As mentioned earlier, GP Industries’ net debt is more than its net cash, and free cash flow is not exactly trending up. Also with a EPS growth (5 years) at negative 3.1, what intrinsic value are we talking about? Nevertheless let’s do a quick study on intrinsic value.

Intrinsic Value

First let’s look at the estimated 5 years earning growth. We are going to use a time-frame of 5 years from now for this purpose (don’t have the 10 years figures). Given EPS and a PE ratio, stock price can easily be calculated for any company. Using the below formula. (actually I just got the results after keying in the figures in this website) F = P(1+R)N where:

- F = the future EPS

- P = the starting (present) EPS (0.05)

- R = compound growth rate (-3.1)

- N = number of years in the future (5)

Estimated future EPS: 0.0427

I will be estimating the future PE of GP Industries to be 24 (See data from Morningstar. I think a P/E of 1,480.7 is too crazy & unrealistic).

Future Stock Price

P=EPSxPE

- P = future stock price

- EPS = future EPS

- PE = future PE

Hence future stock price of GP Industries is 0.0427 x 24 = 1.0248

Intrinsic Value

P=F/(1+R)N

- P = present (intrinsic) value

- F = future stock price (1.0248)

- R = MARR (15% or 0.15)

- N = Number of years (5)

Hence, the intrinsic value of GP Industries is 0.51.

Stock price of GP Industries on 16 July 2015 is 0.73. There is no margin of safety and percentage difference between the intrinsic value and current stock price is 43%!

Nevertheless, GP Industries recently announced in May 2015 that earnings attributable to shareholders of $1.5 million for the fourth quarter is an improvement from the loss of $23.7 million a year back.

GP Industries back in the black for fourth quarter. (read here)

I could be missing something here. The increase in profit was attributable mainly to higher sales, improved margin and exchange gain, despite higher distribution costs and marketing costs partly due to a higher level of brand building activities.

GP does seem to be doing their best in improving sales, but I would like to see a longer track record with consistent good results. To really tell if their strategy is working. Not an insider here.

In summary:

I do not comprehend the rationale behind GP’s management’s numerous share buybacks (in so many consecutive days). It nevertheless caught my attention. Always wonder why they do not space out the buying, and buy on dips.

Although their fourth quarter financial result is an improvement, the past quarterly and yearly financial results have been erratic.

Base on price/book & EV/EBITDA ratios, the company may appear undervalued, however the growth portion is questionable (there is no consistent performance over the years).

GP’s management is aware of the future challenges and sounded cautionary (read here). As stated in the recent fourth quarter report, they highlighted that “Market demand in Europe and some parts of Asia remained weak. Market demand for some of GP Industries Group’s products has started to soften in China. However, GP Industries Group’s businesses in the US remain stable.”

Finally, I feel that the share buy backs do not really add value to the share holders and the money would be better used to pay back the debts (if can’t use it for R&D or expansion).

The stock sale is not here yet….

Thanks for the in-depth analysis of GP Industries. It definitely looks like it is over-priced at the moment!

LikeLike

You are welcome.

LikeLike

Pingback: A Pen Quotes